Blog

Measure what matters: Priority pathways and Creative Higher Education

Bernard Hay, Creative PEC's Policy Director, investigates the surprising absence of creative subject…

11 actions for the cultural and creative industries in the age of AI

A guide to help the cultural and creative industries address the rise of AI, from the GCEC.

Creative Resilience in Times of Crisis

Introducing A Global Agenda for Creative Resilience, an 11-point strategic framework for strengtheni…

Reporting from the Creative PEC Research Symposium 2026

Bringing people together from across academia, industry, and government for discussion and debate on…

Keeping creative options open for everyone

How does creative study allow us to express ideas, shape how we see the world, and contribute to vib…

Coworking spaces as informal skill ecosystems for the creative workforce

How coworking spaces have become an increasingly important component of the creative economy.

From Wales to the World: Why International Cultural Policy Needs a Future Generations Lens

Can international cultural policy be shaped by focusing on future generations?

10 facts about Creative Industries growth potential

Discover ten key findings from the report 'High-Growth Potential Firms in the UK's Creative Industri…

Why London is investing in Creative Enterprise Zones

London Mayor Sir Sadiq Khan announces £2.2 million in new funding for Creative Enterprise Zones.

Research resources on Creative Clusters

We’ve collated recent Creative PEC reports to help with the preparation of your Creative Cluster bid…

What UK Job Postings Reveal About the Changing Demand for Creativity Skills in the Age of Generative AI

The emergence of AI promises faster economic growth, but also raises concerns about labour market di…

Creative PEC’s digest of the 2025 Autumn Budget

Creative PEC's Policy Unit digests the Government’s 2025 Budget and its impact on the UK’s creative …

Why do freelancers fall through the gaps?

Why are freelancers in the Performing Arts consistently overlooked, unseen, and unheard?

Insights from the Labour Party Conference 2025

Creative PEC Policy Adviser Emily Hopkins attended the Labour Party Conference in September 2025.

Association of South-East Asian Nations’ long-term view of the creative economy

John Newbigin examines the ASEAN approach to sustainability and the creative economy.

Take our Audience Survey

Take our quick survey and you might win a National Art Pass.

Culture, community resilience and climate change: becoming custodians of our planet

Reflecting on the relationship between climate change, cultural expressions and island states.

Cultural Industries at the Crossroads of Tourism and Development in the Maldives

Eduardo Saravia explores the significant opportunities – and risks – of relying on tourism.

When Data Hurts: What the Arts Can Learn from the BLS Firing

Douglas Noonan and Joanna Woronkowicz discuss the dangers of dismissing or discarding data that does…

Rewriting the Logic: Designing Responsible AI for the Creative Sector

As AI reshapes how culture is made and shared, Ve Dewey asks: Who gets to create? Whose voices are e…

Reflections from Creative Industries 2025: The Road to Sustainability

How can the creative industries drive meaningful environmental sustainability?

Creating value: the creative economy beyond culture by Marta Foresti

Marta Foresti explains the value of international cooperation as she becomes Chair of the GCEC.

Taking stock of the Creative Industries Sector Plan

We summarise some of the key sector-wide announcements from the Creative Industries Sector Plan.

Conversations between the Global North and South

Unsettling and reordering the creative economy

Why higher education matters to the arts, culture and heritage sectors

Professor Dave O’Brien, Professor of Cultural and Creative Industries at University of Manches…

What does the 2025 Spending Review mean for the creative industries?

A read out from Creative PEC Bernard Hay and Emily Hopkins On Wednesday 11th June the UK Government …

Bridging the Imagination Deficit

The Equity Gap in Britain’s Creative Industries[1]. by Professor Nick Wilson The creative industries…

Why accredited qualifications matter in journalism

Journalism occupations are included on the DCMS’s list of Creative Occupations and, numbering around…

All Together Now?

Co-location of the Creative Industries with Other Industrial Strategy Priority Sectors Dr Josh Siepe…

The Mahakumbh Mela, India, 2025

The festival economy: A Priceless Moment in Time Worth GBP 280 Billion in Trade Jairaj Mashru looks …

Class inequalities in film funding

Professor Dave O’Brien, University of Manchester, Dr Peter Campbell, University of Liverpool and Dr …

Creative self-employed workforce in England and Wales

Dr Ruoxi Wang, University of Sheffield and Bernard Hay, Head of Policy at Creative PEC Self-employed…

What just happened to funding for culture in Scotland?

First the facts: Creative Scotland announced the outcome of its new Multi-Year Funding Programme on …

Copyright and AI – a new AI Intellectual Property Right for composers, authors and artists

Background The new technology landscape emerging from the super rapid progress in developing AI, Gen…

Creative PEC: A Year in Review

Looking back at Creative PEC in 2024 – a year of policy, research and industry achievements, events,…

Measuring the economic value of digital culture

What are consumers are willing to pay for digital streaming services, and how do we measure it?

Lifelong learning in the creative industries, part 2: the solutions

In part 2 of the blog, our Industry Champions discuss possible solutions to the challenges of lifelo…

Lifelong learning in the creative industries – part 1: the challenges

Our Industry Champions discussed the challenges faced in creative industries education and lifelong …

Creative Corridors: Connecting Clusters to Unleash Potential

Introducing the Creative Corridors framework.

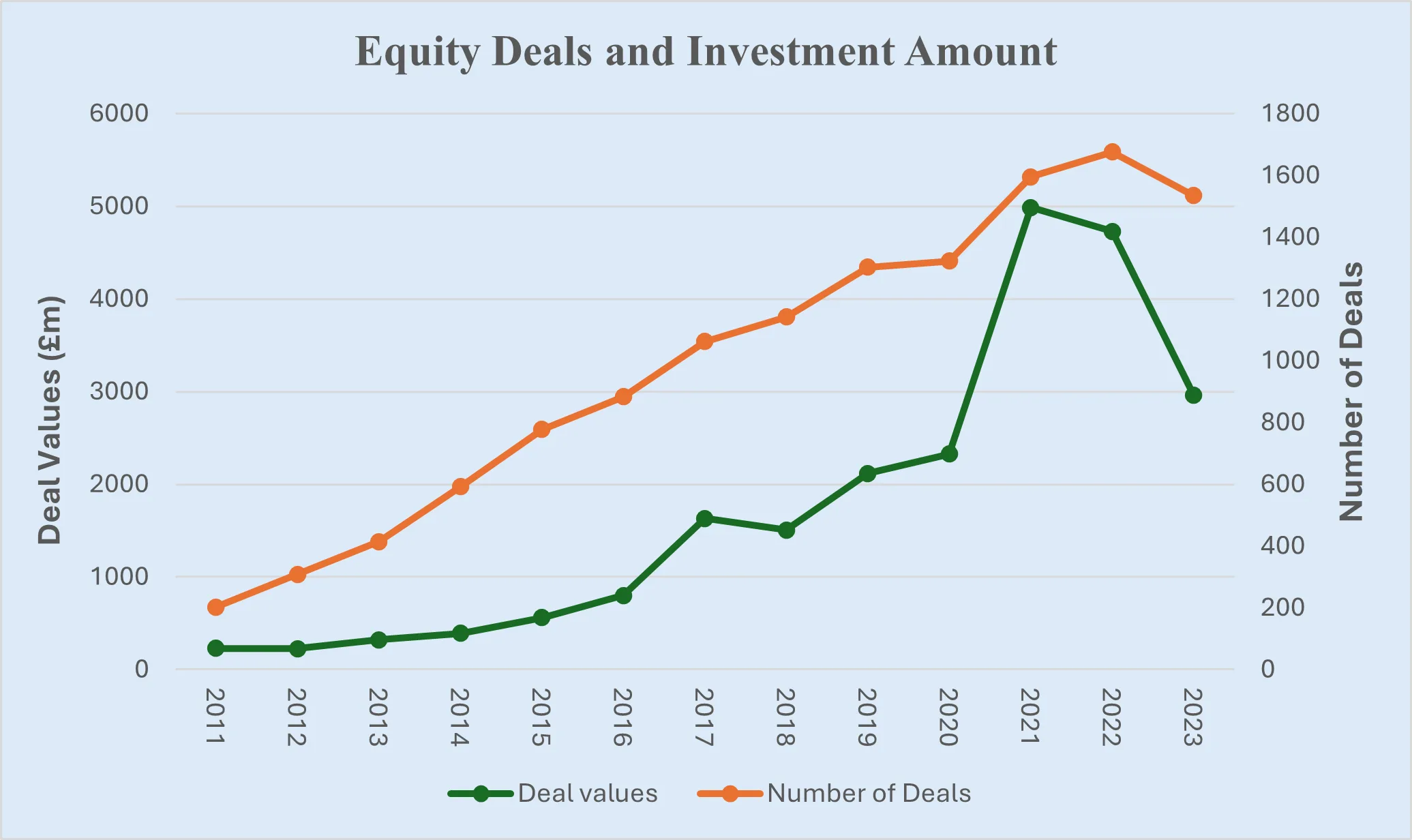

Creative UK Access to Finance Survey: Share Your Views

Professor Hasan Bakhshi, Director Creative PEC and Josh Siepel, Research Lead, R&D, Innovation a…

Unlocking the power and potential of the U.S. creative industries

Cellist Yo-Yo Ma in conversation with Upstart Co-Lab Founding Partner Laura Callanan at “Inves…

Reflecting on a year of State of the Nations reports

We’ve now published a full cycle of our new ‘State of the Nations’ series – which use th…

Copyright protection in AI-generated works: Evolving approaches in the EU and China

Prof Kristofer Erickson discusses the different approaches the EU and China have taken in response t…

Introducing the World Creativity Organization

Edna dos Santos-Duisenberg (member of Creative PEC's Global Creative Economy Council) & Lucas Foster…

Island in Transition: The Journey from Reggae Music Mecca to Creative Economy Hub

Andrea Dempster Chung, Co-founder and executive director of Kingston Creative A blog from Creative P…

UK engagement in Central Asia: Education and the creative economy in the territories of the ‘new Silk Roads’

Dr Martin Smith and Dr Gerald Lidstone look at the history of the British Council's work in Central …

Creative Industries in Egypt: An Overview

Omar Nagati – GCEC Member and Co-Founder of CLUSTER – outlines the findings of a study into the crea…

Hasan Bakhshi and Rehana Mughal introduce the Global Creative Economy Council

Hasan Bakhshi and Rehana Mughal explain what the GCEC is trying to achieve and how the network will …

Global Creative Economy Council: An introduction from the Former Chair

John Newbigin introduces Creative PEC's Global Creative Economy Council

Creative PEC’s response to the Spring Budget 2024

Creative Industries in the 2024 Spring Budget The creative industries are a significant part of the …

Copyright protection in AI-generated works

Timely exploration of copyright law and AI generated creative content

The economic value of cinema venues to their communities

In a tough economic climate for cinemas and where there is limited public funding, it is important t…

Creative diversity in higher education

As the APPG for Creative Diversity launches their annual report, ‘Making the Creative Maj…

Estimating the Contribution of Arts, Humanities and Social Sciences (AHSS) R&D to Creative Industries R&D

The UK’s creative industries are hugely innovative; PEC research has suggested that over two-th…

The Media Bill and the future of Public Service Broadcasting policy

In March the government published the first draft of its long-awaited Media Bill. The Bill prop…

Creative spillovers: Do the creative industries benefit firms in the wider economy?

The creative industries are a force for innovation in the UK. Firms in the creative industries (CIs)…

The PEC’s response to the 2023 Spring Budget

The creative industries are a vital part of the UK economy. There are, however, some continued chall…

Re-imagining Channel 4’s Future

Michelle Donelan, the Secretary of State for Digital, Culture, Media & Sport, has formally …

A new deal for arts funding in England?

When thinking about why we publicly fund the arts, we can point to their multifaceted benefits. Not …

Too many demands are being placed on universities to support their regional economies, without sufficient support and partnership

The creative industries have long been heralded as a UK success story. The creative economy grew at …

Can you own a pixel?

This blog is based on the discussion paper Crypto Art and Questions of Value, a guide for anyon…

What the Autumn Budget means for the Creative Industries

With the UK almost certainly entering a recession – Q3 has seen negative GDP growth – and inflation …

Trade in creative services: scale, trends, and geography

Creative services such as advertising, publishing, and design are an important part of global trade.…

How data analysis of colour can help courts make objective decisions about trademarks

The overall appearance of a product or service is called ‘trade dress’, according to trademark law. …

How a placed-based employment programme is bringing creative workers back to Northern Ireland

The Department for Communities (DfC) recently awarded £4.7 million to Future Screens NI (F…

New research suggests regulation could actually enhance user-creativity on the platform giants

Video-sharing platforms such as YouTube, Vimeo, and TikTok provide a free space for everyone to shar…

How Research and Innovation can help level-up the Creative Industries

The Levelling-Up White Paper produced by the Department for Levelling-Up, Housing and…

Creative Clusters Case Studies

Creative Clusters – Case Studies The creative clusters in these case studies share some common…

How to find out more about your local Creative Industries

How those bidding for levelling up funds can find out more about their local Creative Industries Alt…

Eight things to know about the Creative Industries

What are the Creative Industries? The Creative Industries are a diverse and complex sector made up o…

Class inequality in the Creative Industries is rooted in unequal access to arts and cultural education

There is an incoherence at the heart of government policy. While Culture Secretary Nadine Dorries is…

How can policy makers help rural creative businesses contribute to Levelling Up?

The creative industries have the potential to play a major role in the development of rural communit…

Channel 4: Streaming on the world stage? Competing in the Changing Media Landscape

On April 28th, ‘The Government’s Vision for the Broadcasting Sector’ (CP 671) was published. The Whi…

Envisioning Broadcasting Anew: the future of UK broadcasting policy

Last week the Department for Digital, Culture, Media and Sport (DCMS) released its long-awaited …

Privatising Channel 4: The evidence behind the debate

On April 4th the government confirmed its plans to privatise Channel 4, the UK’s publicly …